New Zealand property valuation 2025: Complete Guide for Homeowners

TL;DR Summary

- National house prices stabilised in 2025, with Stats NZ reporting a median value of $790,000 in June, showing modest growth since 2023 (Stats NZ).

- Rateable Values (RVs) remain for rating only, with Auckland Council confirming they are updated every three years and do not reflect real-time sale prices (Auckland Council).

- Borrowing costs shifted significantly, as the Reserve Bank of New Zealand lowered the OCR to 3.0% in August 2025, stimulating buyer activity (RBNZ).

- Housing supply tightened, with Stats NZ reporting a 6.4% decline in building consents in June 2025, impacting property availability (Stats NZ).

- Professional appraisals offer clarity, with Price My Property providing free, suburb-specific valuation reports that combine official data with local expertise (Price My Property).

New Zealand property valuation 2025 is more than just a figure—it is the foundation for confident decisions in selling, refinancing, and investment planning. With property markets stabilising after years of volatility, homeowners in 2025 need valuations that not only capture today’s value but also anticipate the dynamics of interest rates, buyer demand, and housing supply.

Strong valuations matter because they underpin every financial choice a homeowner makes. Stats NZ reports a national median house price of $790,000 as of June 2025, but this figure alone doesn’t tell the story of individual suburbs, renovated homes, or unique lifestyle blocks. Similarly, Auckland Council’s Rateable Values are useful for rating purposes, yet they cannot predict what buyers are currently willing to pay. This gap between official data and market reality is where professional appraisals play a critical role.

That’s where Price My Property bridges the divide. By combining government benchmarks with agent expertise, the platform delivers free market valuation reports that provide more than numbers—they offer strategy. Each appraisal includes comparable sales, suburb-level insights, and personalised recommendations on timing and marketing. For homeowners preparing to sell in 2025, this is the clearest way to move from data to action.

Why property valuation matters in 2025

New Zealand property valuation 2025 is essential because it directly influences how homeowners, buyers, and lenders make decisions. In a year defined by stabilising house prices and lower interest rates, understanding your home’s real value has never been more critical.

For sellers

Homeowners looking to sell in 2025 must know where their property sits in the market. Stats NZ reports the national median house price reached $790,000 in June 2025, but that broad number hides wide variations between suburbs. A tailored valuation ensures sellers price competitively without leaving money on the table.

For refinancers

Banks rely on defensible figures before extending credit. Most lenders require a registered valuation, but an initial market appraisal helps homeowners assess whether refinancing is worth pursuing. An accurate property valuation can reveal equity that supports debt consolidation, renovations, or investment purchases.

For investors

The Ministry of Housing and Urban Development (HUD) notes that investor demand shifts with tenancy reforms and tax settings. Valuations give investors insight into rental yields, equity growth potential, and capital gains exposure. In 2025, when affordability challenges persist, valuations help investors align portfolios with government policy and market signals.

For everyday homeowners

Even without immediate plans to sell, a valuation can guide major financial decisions. Renovation projects, estate planning, or simply understanding net worth all begin with knowing the current value of your property. New Zealand property valuation 2025 ensures homeowners stay informed and proactive in managing their most valuable asset.

CTA: Thinking about your next move? Request your free appraisal from Price My Property and turn today’s numbers into tomorrow’s strategy.

Valuation methods in New Zealand property valuation 2025

Property valuation 2025 relies on several approaches, each designed for different purposes. From quick online tools to formal registered reports, choosing the right method depends on whether you’re selling, refinancing, or planning.

Automated Valuation Models (AVMs)

Automated Valuation Models draw on recent sales and government datasets such as those published by Stats NZ. They are fast, free, and accessible online, providing a ballpark estimate within seconds. However, AVMs often miss property-specific details such as renovations, unique layouts, or desirable outlooks. For many homeowners, AVMs are a starting point—not the final word.

Rateable Values (RVs)

Councils like Auckland Council update RVs every three years to determine rates. The last Auckland revaluation took effect on 1 May 2024, with new values applied to rates bills from 1 July 2025. While RVs provide a benchmark for local authorities, they are not intended to reflect current market value. A home may sell for significantly more or less than its RV, depending on market conditions and buyer demand.

Registered Valuations

Registered valuations are formal, lender-grade reports completed by independent valuers. They are typically required by banks for refinancing or high-value lending decisions. A registered valuation considers property condition, comparable sales, and broader economic factors. While highly reliable, they come with costs ranging from $500 to $1,000 or more and usually take several days to complete.

Licensed Agent Appraisals

For homeowners preparing to sell, licensed agent appraisals offer the most practical insights. Through Price My Property, sellers can access free appraisals from top-performing agents who combine local market knowledge with government data. These reports not only estimate value but also provide advice on timing, presentation, and marketing strategy—making them a powerful tool for maximising outcomes in 2025.

CTA: Ready to compare the numbers? Book your free appraisal with Price My Property and see how your home stacks up.

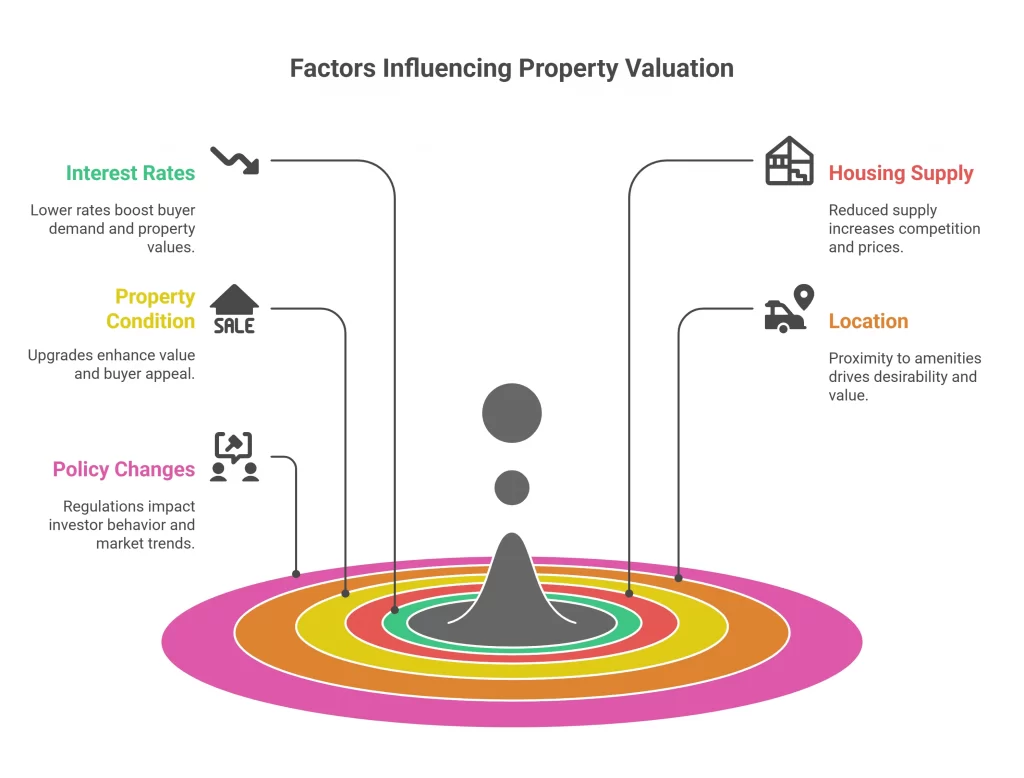

Factors influencing property valuation 2025

New Zealand property valuation 2025 is shaped by a mix of economic, physical, and regulatory factors. While some are within a homeowner’s control, others depend on broader market conditions and government policy.

Interest rates and credit conditions

The Reserve Bank of New Zealand lowered the Official Cash Rate (OCR) to 3.0% in August 2025. This decision reduced borrowing costs and boosted buyer demand, particularly among first-home buyers and upgraders (RBNZ). Lower interest rates often increase property valuations because more buyers can afford higher mortgages, thereby pushing up competition.

Housing supply and building activity

Stats NZ reported a 6.4% fall in building consents in June 2025 following a sharp rise in May (Stats NZ). Reduced new supply means buyers face fewer choices, which typically strengthens property values in established suburbs. For sellers, this creates opportunities to achieve premium results when supply is tight.

Property condition and compliance

Renovations, maintenance, and compliance play a major role in valuations. Homes upgraded with energy-efficient features, modern kitchens, or Healthy Homes standards often achieve 5–15% higher valuations compared with similar unrenovated properties. LIM reports and council consent records also affect value; unconsented works may reduce buyer confidence and lender approval.

Location and infrastructure

Proximity to transport links, schools, parks, and shopping centres continues to be a key driver of value. HUD notes that new zoning rules and housing reforms influence both affordability and desirability. Properties near planned infrastructure projects often benefit from higher valuations as accessibility improves.

Policy and regulation

Legislative changes, such as Bright-Line Test amendments or tenancy reforms, influence investor behaviour. In 2025, government housing policy aims to balance affordability with supply, creating ripple effects in valuation trends. Staying informed through HUD and MBIE ensures that homeowners understand how regulations impact demand.

CTA: Want to see how these factors affect your home? Get your free Price My Property appraisal and understand your true market value.

The benefits of professional appraisals

New Zealand property valuation often begins with quick online estimates, but professional appraisals remain the gold standard for accuracy and strategy. While automated tools and Rateable Values provide rough guides, they can miss the nuances that ultimately drive sale prices.

Limitations of AVMs and RVs

Automated Valuation Models are helpful for early research, but they can deviate by 10–20% from actual sale prices. They struggle with unique properties such as lifestyle blocks, character homes, or recently renovated dwellings. Similarly, Rateable Values from councils like Auckland Council are intended for rating purposes only and may not reflect current buyer demand. These figures are updated infrequently, meaning they lag behind market shifts.

Why professional appraisals outperform

Licensed agent appraisals, such as those offered free by Price My Property, provide insights that raw data cannot. They combine

Comparable sales: Drawn from recent Stats NZ and council records.

Property condition assessments: Factoring in upgrades, maintenance, and compliance. Local buyer trends: Including suburb-specific demand, open-home attendance, and auction clearance rates.

Strategic advice: Timing, pricing strategy, and marketing recommendations tailored to your goals. The value of strategy.

Professional appraisals don’t just answer “what is my home worth?”—they answer “how can I maximise my sale price?” For sellers, that strategy is just as important as the valuation number. By understanding buyer psychology, agent experience, and market timing, homeowners gain a competitive edge.

CTA: Don’t rely on estimates alone—book your free professional appraisal with Price My Property and unlock your property’s full potential.

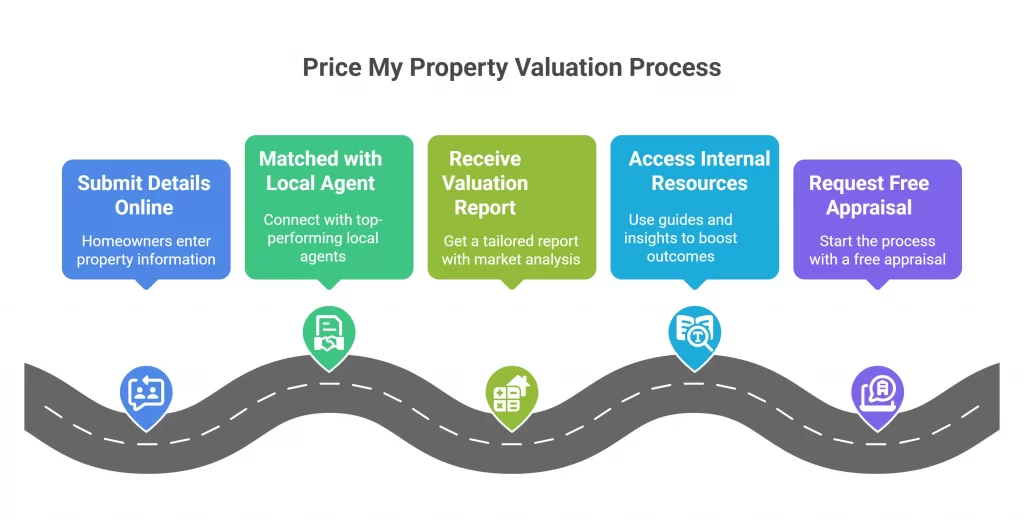

How Price My Property supports sellers

Property valuation In 2025 becomes much easier when homeowners use trusted tools that blend data with expertise. That’s where Price My Property steps in, providing free, suburb-specific appraisals from licensed real estate professionals.

Step 1: Submit your details

The process starts with a simple online form. Homeowners enter their address and property information, such as size, age, and any recent renovations.

Step 2: Get matched with the right agent

Price My Property then connects you with top-performing local agents who specialise in your suburb. Unlike automated platforms, this step ensures that your valuation reflects local buyer behaviour, not just raw statistics.

Step 3: Receive a free valuation report

Within days, you receive a tailored valuation report. This includes:

- Comparable recent sales in your area (drawn from Stats NZ and council records).

- Analysis of local market trends.

- Strategic advice on pricing and marketing for your property.

- Recommendations on timing—crucial in a shifting interest rate environment.

Internal resources to prepare for sale

Price My Property also provides sellers with guides and insights to boost outcomes, including:

- How to Sell Your House — a step-by-step selling roadmap.

- NZ Property Sellers 2025: How to Maximise Your Sale Price — focused on presentation and strategy.

- How Falling Mortgage Rates in NZ 2025 Are Fueling House Sales — analysis on rate changes and demand.

Why sellers choose Price My Property

Unlike AVMs or RVs, these appraisals combine government data with on-the-ground insights, giving sellers confidence in both the number and the plan. For 2025, where demand is shaped by shifting rates and supply constraints, this dual perspective is invaluable.

CTA: Ready to see your home’s true market potential? Request your free Price My Property appraisal today

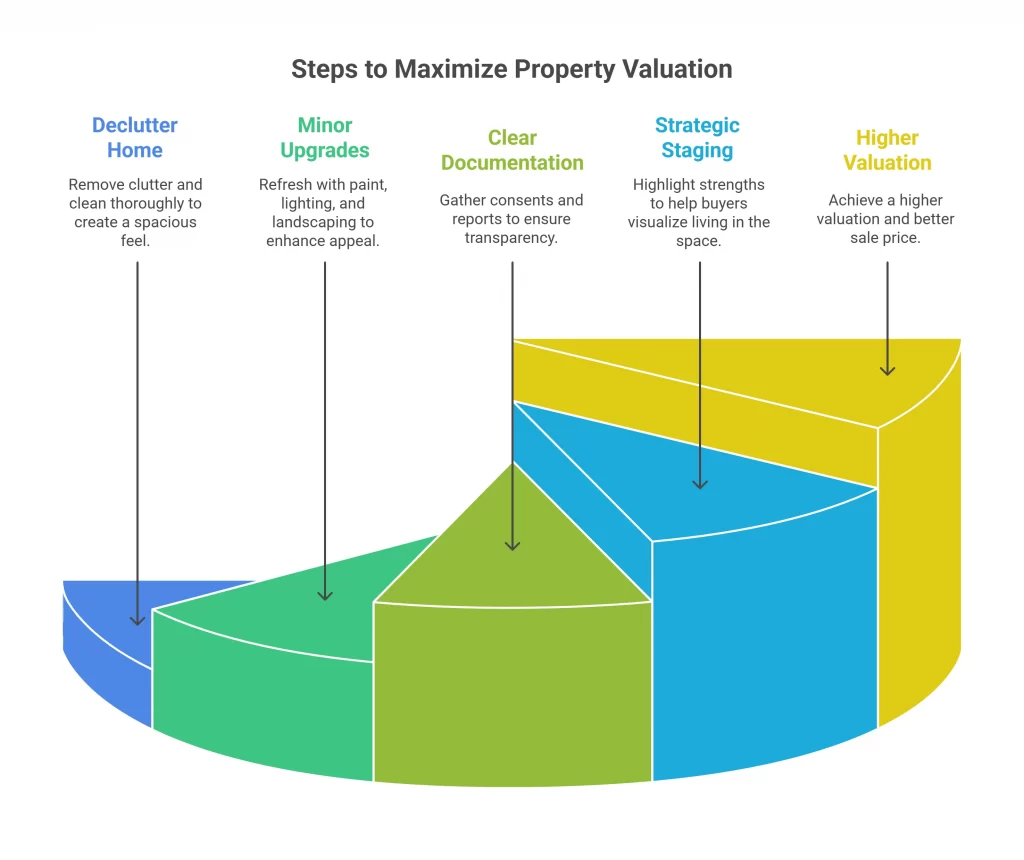

Tips to maximise your property valuation in 2025

New Zealand property valuation 2025 is not fixed—it can be improved by how you prepare and present your home. Sellers who invest time in staging, repairs, and clear documentation often achieve higher valuations and better sale prices.

Declutter and present a tidy home

First impressions matter. Buyers often decide within minutes whether a home feels spacious and well-kept. Removing clutter, cleaning thoroughly, and depersonalising spaces creates a neutral canvas that appeals to a wider pool of buyers.

Make minor upgrades count.

Minor, inexpensive improvements can make a big difference. A fresh coat of paint, modern light fittings, or tidy landscaping can lift appeal without significant costs. These touches can increase a valuation by several percentage points, especially in competitive markets.

Provide clear documentation

Valuers and appraisers rely on evidence. Have council consents, LIM reports, and renovation records ready. Transparency around upgrades reassures buyers and banks, while demonstrating compliance with building standards. MBIE’s Healthy Homes Standards also add confidence for investor buyers when properly documented.

Stage your home strategically.

Professionally staged homes often sell faster and for higher prices. Staging highlights a property’s strengths and helps buyers visualise living in the space. This is particularly powerful in markets where buyer choice is limited, as seen in 2025 with falling building consent numbers.

Case study: How small changes boost value

A Wellington homeowner preparing to sell a 1970s three-bedroom house engaged an agent through PriceMyProperty. Initially, the home’s valuation reflected dated interiors. After two weeks of preparation—painting, garden work, and professional staging—the updated appraisal came in 8% higher. The home eventually sold above the top of the price range, showing how simple steps can deliver strong results.

CTA: Want to know which improvements could lift your valuation? Get your free Price My Property appraisal and receive personalised recommendations.

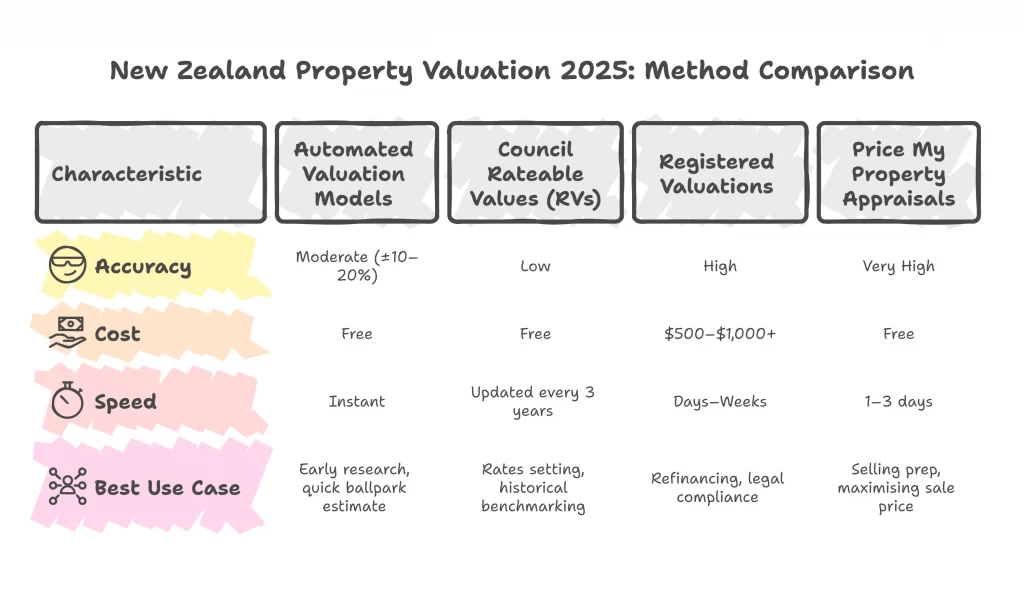

Comparison of valuation approaches

New Zealand property valuation 2025 can be assessed in different ways, each with unique strengths and limitations. Understanding these options helps homeowners choose the right method for their purpose—whether selling, refinancing, or planning ahead.

This comparison shows why homeowners preparing to sell in 2025 increasingly rely on professional appraisals. While AVMs and RVs provide background figures, only a tailored appraisal brings together market data, local demand, and strategic advice.

CTA: Compare your options and choose confidence—book a free Price My Property appraisal today.

Case study — The impact of interest rates on 2025 valuations

Property valuation 2025 is directly influenced by interest rate shifts, which affect both affordability and buyer demand. When the Reserve Bank of New Zealand cut the Official Cash Rate (OCR) to 3.0% in August 2025, borrowing costs fell, and more buyers entered the market (RBNZ).

The numbers behind the trend

Stats NZ reported that national sales volumes rose 4% in Q2 2025 compared to the same period in 2024 (Stats NZ). Auckland’s median property price climbed to $1.02 million, reflecting renewed demand as mortgage repayments became more manageable.

How this played out for sellers

Consider a homeowner in Auckland’s North Shore who sought an appraisal through Price My Property in mid-2025. Prior to the OCR cut, comparable homes in the area were struggling to meet RV benchmarks. Within weeks of the interest rate drop, open-home attendance rose, auction clearance rates improved, and the homeowner’s updated appraisal reflected a 7% higher value range.

Lessons for 2025 homeowners

This case demonstrates that New Zealand property valuation 2025 is not static—it responds to macroeconomic signals. Sellers who time their campaigns around favourable credit conditions can secure stronger results. Professional appraisals that account for both government data and buyer sentiment provide the most precise guidance in such markets.

CTA: Want to know how changing interest rates could affect your home’s value? Request your free Price My Property appraisal today.

FAQ Section

Q1: How accurate are Council Rateable Values in 2025?

A: Council Rateable Values (RVs) are updated every three years and used for rating purposes, not real-time sales. In 2025, the Auckland Council confirmed that RVs are not intended to reflect market value (Auckland Council).

Q2: Can Stats NZ data replace a property appraisal?

A: No. Stats NZ provides national and regional averages, such as the June 2025 median of $790,000; however, it cannot capture the unique features of individual homes (Stats NZ).

Q3: How does the Reserve Bank OCR affect valuations?

A: When the Reserve Bank lowered the OCR to 3.0% in August 2025, mortgage costs fell, increasing buyer demand and pushing up property values (RBNZ).

Q4: Do I need a registered valuation to refinance?

A: Yes. Most banks require a registered valuation from an independent valuer for refinancing, even if you already have an agent appraisal.

Q5: What is the difference between an appraisal and a valuation?

A: A licensed agent appraisal (such as those from Price My Property) provides a market estimate and sales strategy. A registered valuation is a formal, lender-approved report required for mortgages or legal purposes.

Q6: How can I object to my council valuation?

A: Homeowners can lodge an objection to their RV through their council. Auckland Council, for example, provides an online objection process after each revaluation cycle (Auckland Council).

Q7: What role does housing supply play in valuations?

A: Stats NZ reports that building consents fell by 6.4% in June 2025. With fewer new builds entering the market, existing homes face less competition, supporting higher valuations (Stats NZ).

Q8: Are Price My Property appraisals really free?

A: Yes. Price My Property connects homeowners with licensed agents who provide comprehensive, obligation-free appraisals at no cost.

Conclusion

New Zealand property valuation 2025 is more than a number—it’s the key to making smart financial decisions in a shifting market. While government sources, such as Stats NZ, the Reserve Bank, and Auckland Council, provide essential benchmarks, they don’t capture the full story of your home’s unique value.

That’s why personalised, professional appraisals are so important. By combining official data with local expertise, Price My Property enables homeowners to see beyond the averages and understand their property’s true potential. Whether you’re selling, refinancing, or simply planning, a tailored appraisal gives you the confidence to act strategically.

CTA: Don’t leave your property’s future to guesswork—book your free expert appraisal with Price My Property today and discover your home’s true value in 2025.

Methodology

This article on New Zealand property valuation 2025 was developed using only New Zealand government and official sources to ensure accuracy and reliability:

- Stats NZ — for national and regional house price medians, housing affordability, and building consent statistics.

- Reserve Bank of New Zealand (RBNZ) — for Official Cash Rate (OCR) announcements and monetary policy impacts on the property market.

- Auckland Council — for Rateable Values (RVs), revaluation cycles, and information on rating policy.

- Ministry of Business, Innovation and Employment (MBIE) – Tenancy Services — for Healthy Homes Standards and rental compliance.

- Ministry of Housing and Urban Development (HUD) — for housing policy updates, supply strategies, and affordability insights.

- Land Information New Zealand (LINZ) — for property titles, zoning, and the Landonline system.

Internal insights and homeowner case studies were drawn from Price My Property resources, including guides on selling, maximising sale price, and responding to mortgage rate changes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}