How to Get a Free House Valuation in NZ (and When to Pay for One)

TL;DR

- A written appraisal must be provided before you sign an agency agreement, and it has to reflect market evidence — it is not a formal valuation. Settled.govt.nz

- Only registered valuers can issue formal valuations under the Valuers Act 1948. New Zealand Legislation

- Rating valuations (CV/RV) are for setting council rates, and the system is regulated by the Valuer-General at Toitū Te Whenua/LINZ — they are not the same as market value.

- Banks manage mortgage risk using loan-to-value ratio (LVR) settings and may require a bank-accepted valuation to confirm security value. Reserve Bank of New Zealand

- For market context, lean on official statistics (e.g., property series from Stats NZ) alongside evidence for the specific home you’re pricing. Stats NZ

Why value clarity matters before you list or borrow

Getting an accurate number starts with understanding three different concepts: an appraisal, a registered valuation, and a CV/RV. An appraisal is a written estimate of the likely sale price based on comparable sales and current market conditions; it’s required before you sign an agency agreement and helps set pricing strategy, but it isn’t a legal valuation. A registered valuation is a formal report prepared by a registered valuer, typically relied on for lending decisions, refinancing, complex properties, or legal contexts. A CV/RV is a mass-appraised rating value used by councils to set rates. It can lag behind fast-moving markets, so it should be used as context — not as a price tag.

Set expectations early: lenders decide what evidence they’ll accept, registered valuations take time and cost money, and even free estimates should be sanity-checked against recent, like-for-like sales. If you’re at the “what’s my place worth?” stage and want a safe starting point, Free House Valuation in NZ tools are best used as a first pass before engaging agents or your bank.

Start with a quick estimate tailored to your address at Price My Property

Appraisal, valuation, and CV/RV explained

Appraisal

Start with clarity: An appraisal is a written estimate of the likely sale price prepared by a real estate licensee professional to help you set expectations and a pricing strategy before signing an agency agreement. A quality appraisal clearly explains how your home compares with recent, like-for-like sales and why the suggested price range is realistic in current conditions. It should be in writing, supported by comparable sales evidence, and tailored to your property—not a generic print-out. The Real Estate Authority

Registered valuation (who can issue, when it’s required, acceptance)

Legal status matters: A registered valuation is a formal report that can only be issued by a registered valuer under the Valuers Act 1948. Lenders, courts, and some councils rely on this level of assessment because the valuer is professionally accountable and must follow recognised standards and methodology. You’ll typically need a registered valuation for lending (refinance, construction, low-deposit scenarios), complex or unique properties, or legal processes where an evidence-based market value is required.

CV/RV (how they’re produced, audit cycle, why they can lag market value)

Rates tool—not a price tag: Rating valuations (CV/RV) are mass appraisals produced for councils to set rates, and they’re overseen and audited nationally by the Valuer-General to ensure consistency with the Rating Valuations Rules. Because they’re generated on a set cycle and at scale, CVs often lag fast-moving markets and may not capture recent renovations or local shifts—use them as context alongside current sales evidence rather than as a sale price target. LINZ

The free options (and how to use them wisely)

Online estimates — strengths, blind spots, and how to reality-check with recent comparable sales.

Great for first look, not final say: Free online estimates can quickly triangulate a ballpark based on past sales and public records, but they struggle with features the data can’t “see” (recent upgrades, unique design, development potential). Reality-check every estimate against recent, nearby, like-for-like sales and note any justified adjustments (floor area, land size, condition, outlook). That aligns with regulator guidance: value opinions should be grounded in comparable information rather than assumptions

Agent appraisal/CMA — what your written report should include

Demand the evidence: A robust comparative market analysis (CMA) will show:

- Like-for-like sales with address, sale date, and key attributes

- Adjustments explaining differences (area, garaging, section, condition, school zones)

- Active and withdrawn listings to indicate competition and buyer depth

- Time on market indicators to manage expectations

This written appraisal must realistically reflect current market conditions and be backed by relevant data—not just a price promise.

Using your CV/RV as context only — when it helps, when it misleads.

Treat it as a reference point: Your CV/RV can help frame suburb norms and council records, but because the Valuer-General’s system is designed for rating—not individual sale pricing—it can mislead where markets move quickly or renovations are recent. Cross-check CVs with up-to-date comparable sales and a written appraisal before anchoring expectations.

Get a consolidated starting estimate before speaking to a bank or agent at Price My Property.

When you should pay for a valuation

Lending triggers — purchases, refinancing, construction loans, low-deposit scenarios

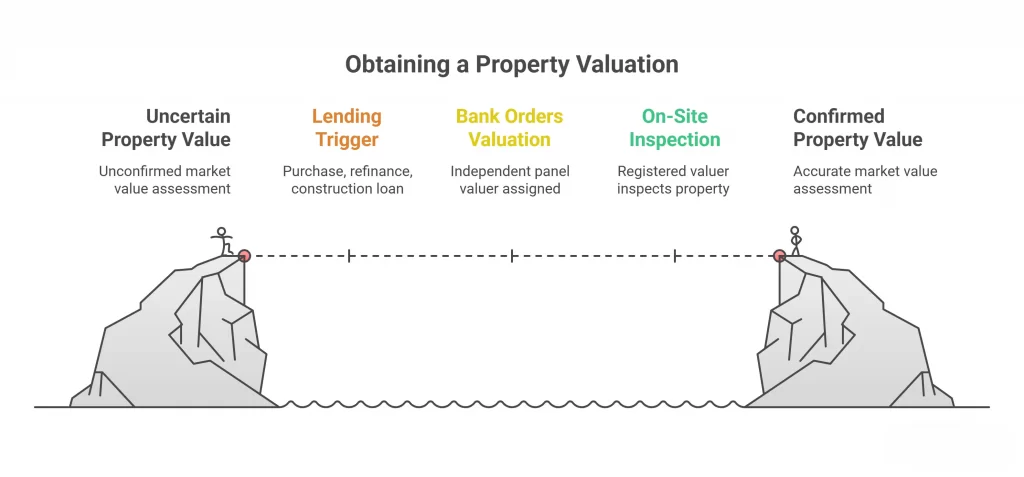

Big picture: banks assess security value against risk tools like loan-to-value ratio (LVR) and debt-to-income (DTI) settings, so they may require an independent valuation to confirm market value. Expect this when you’re buying, refinancing, building, topping up for renovations, or borrowing with a small deposit. LVR limits were eased alongside the introduction of DTI on 1 July 2024, but lenders still need reliable valuations to evidence equity and serviceability under these rules. Reserve Bank of New Zealand

Who orders it and why (bank-accepted processes; independence and panels)

Independence matters: for lending, valuations are typically ordered by your bank or broker through a bank-approved platform that assigns an independent panel valuer. This preserves arm’s-length objectivity and ensures the report format, data sources, and quality checks match the lender’s requirements. You’ll receive a payment link; an independent panel valuer is assigned via the bank’s platform; the report is released to you and the bank.

Property types that defeat models (unique/rural/new builds/subdividable sites)

When a human beats the algorithm: automated or mass-appraisal approaches struggle when a home has limited comparable sales, recent bespoke upgrades, rural or lifestyle features, brand-new construction, or development potential (e.g., subdividable land). In these cases, a registered valuation grounded in on-site inspection and comparable evidence is the safer route for pricing and lending decisions. Government guidance also reminds sellers and buyers that modelled or rating values are not the same as the current market value.

Typical NZ costs, timeframes, and validity windows (what affects price and speed)

What to expect: registered valuation fees vary by location, urgency, and complexity (unique/rural sites or multi-dwelling properties cost more). Turnaround is commonly 4–15 working days, depending on access and scope, and many lenders treat reports as current for about three months, after which they may seek confirmation or a fresh report. Check your finance dates to avoid expiry.

Get a Free House Valuation in NZ and estimate before speaking to a bank or agent at Price My Property

Decision tree — from the first click to the right number in 48 hours

Day 0 (Hour 0–2): Set your baseline

- Enter your address and key details (beds, baths, floor area, section size, recent renovations, consented works) to generate a starting estimate.

- Save notes on unique features (sun, outlook, school zones, garaging) and any detractors (deferred maintenance, road noise).

- Gather recent documents: LIM/building report (if available), plans, code compliance, rates notice, rental evidence (if investment).

Choose your path

Branch A — Selling

- Request two independent written appraisals (Hour 2–12): Ask each agent for like-for-like comparables, adjustments, and time-on-market guidance.

- Stress-test the ranges (Hour 12–24): Compare each appraisal against the latest settled sales within 3–6 months and within a similar micro-market. Query any outliers.

- Set a pricing strategy (Hour 24–36): Align the method of sale with your timeframes and risk tolerance (auction, deadline, price by negotiation).

- List readiness (Hour 36–48): Organise photography, marketing copy, and disclosure pack so you can move from appraisal to live listing without delay.

Branch B — Borrowing

- Confirm lender requirements (Hour 2–8): Ask your bank/broker which valuation type they will accept, who orders it, the fees, and the validity period.

- Order promptly (Hour 8–12): Expect the bank to instruct a panel valuer; pay the fee and arrange access. Provide plans, consent records, and renovation invoices to speed things up.

- Track the critical dates (Hour 12–36): Align finance/conditional dates with expected turnaround; if timing is tight, request urgency early.

- Close the loop (Hour 36–48): Review the report for assumptions and comparables. If the value is short, discuss equity/LVR impacts and next steps with your lender.

Branch C — Just curious

- Baseline now (Hour 0–2): Generate an estimate and record key property notes.

- Monitor suburb trends (Hour 12–36): Keep an eye on recent local sales and open-home chatter to understand buyer depth.

- Reassess quarterly (Hour 36–48+): Re-estimate after material market moves or after you complete improvements.

48-hour checklist

- Baseline estimate saved

- Two appraisals requested (if selling) or lender requirements confirmed (if borrowing)

- Documents assembled (plans, consents, LIM, invoices)

- Timeframes aligned with valuation/report delivery

Follow the steps with your own address at Price My Property and get a guided action plan tailored to your situation.

Accuracy check — how to sanity-test any estimate

Selecting proper comparables

- Start with time: prefer sales from the last 3–6 months; stretch only if the local sales pool is thin and note why.

- Stay close: pick sales from the same micro-market (school zone, street character, transport links) because suburb-wide medians can mask big pockets of difference.

- Match property type: compare house with house, townhouse with townhouse, apartment with apartment; avoid mixing freehold with leasehold.

- Normalise land and floor area: align on section size, floor area, bedroom/bathroom count, garaging, and outdoor flow.

- Control for condition: renovated vs original, double-glazing, insulation, heating, cladding, and weathertightness history all matter.

- Mind the method of sale: auction vs deadline vs private treaty can influence headline prices; weight results accordingly.

- Check legal context: cross-lease vs freehold, easements, covenants, and consent status can swing value even within the same street.

Making defensible adjustments (floor area, section, condition, improvements)

- Bracket your subject: pick one slightly superior and one slightly inferior comparable, then explain your adjustments back to the middle.

- Explain every change: if you adjust for floor area, section size, bed/bath mix, parking, outdoor living, or view/sun, state the rationale in plain English (e.g., “+ value for internal access double garage”).

- Condition & improvements: distinguish maintenance (restores value) from capital improvements (adds value). Provide invoices/consent numbers so the adjustment is evidence-based.

- Market tempo: factor in days on market and buyer depth; a quick, multi-bid sale may justify less discounting than a property that lingered.

- Keep an audit trail: save links to settled sales, photos, and sale methods so a banker, buyer, or valuer can reproduce your logic.

Red flags (anchoring to CV, outlier comps, ignoring days on market)

- Anchoring to CV/RV: rating values are for rates, not current market value; treat them as context only.

- Cherry-picked outliers: a single record price or distress sale shouldn’t anchor your range; look for a cluster of corroborating sales.

- Listing prices, sale prices: advertised asks and RVs can mislead—use settled sales first.

- DOM blindness: Ignoring days on market and vendor discounting can inflate expectations.

- Scope creep: mixing apartments, townhouses, and stand-alone houses in one analysis undermines like-for-like integrity.

- Unverified upgrades: unconsented works or undocumented renovations should not attract full value adjustments.

Market pulse — reading official stats the right way

Zoom out, then zoom in: start with official releases to frame national settings, then translate those signals to your neighbourhood using recent comparable sales.

Use the right dials:

○ Stats NZ: population flows, building consents, rental and construction cost indexes help explain supply–demand pressure.

○ Reserve Bank of New Zealand: Official Cash Rate, mortgage rate trends, and lending data (including LVR/DTI) show credit conditions that shape buyer capacity.

○ Toitū Te Whenua/LINZ: information on the rating valuation system and revaluation cycles helps you understand why CVs can diverge from sale prices.

- National vs local: national indexes move slowly; your suburb can run hotter or cooler depending on new supply, school zoning, big employers, or transport upgrades. Always reconcile national direction with street-level evidence from recent settled sales.

- Don’t overreact to monthly noise: look for rolling multi-month trends and seasonality (holidays, winter slowdowns). Small samples can cause sharp monthly swings—avoid rewriting your price view on one data point.

- Build a simple dashboard: track OCR changes, average fixed mortgage rates, quarterly population estimates, monthly building consents, and a handful of very recent local sales. If the macro dials tighten (higher rates, softer population growth) yet your micro-market shows strong competition, weight decisions to the local evidence—but document why.

- Turn stats into strategy: if credit conditions ease and local days-on-market shorten, you may price closer to the upper end of your range; if rates rise and buyer depth thins, consider sharper pricing or more time to sell.

Regional snapshots (Auckland, Wellington, Christchurch, Tauranga, Dunedin)

Auckland

- What typically triggers paid valuations: Complex builds, subdividable sections, significant renovations, or low-deposit lending often prompt lenders to request a registered valuation. Intensification rules under the Auckland Unitary Plan can add development potential that AVMs don’t capture well. new.aucklandcouncil.govt.nz

- CV recency & planning settings: Auckland’s 2024 general revaluation is dated 1 May 2024 and is used to set rates from 1 July 2025—helpful for context, but not today’s market value. Recent plan changes responding to the NPS-UD can materially alter site potential, so don’t anchor to older CVs.

Wellington

- What typically triggers paid valuations: Steep sites, earthquake-strengthening considerations, character areas, and bespoke renovations reduce the reliability of modelled estimates; lenders may ask for a registered valuation, especially for refinancing or new builds.

- CV recency & planning settings: The latest rating revaluation uses an effective date of 1 September 2024; anything after that won’t be reflected. Proposed District Plan intensification (e.g., Medium Density Residential zones) can change highest-and-best-use assumptions, skewing expectations if you rely on older CVs. wellington.govt.nz

Christchurch

- What typically triggers paid valuations: Large sections, post-quake rebuild/repair histories, and lifestyle edges around the city often require a formal valuation for lending.

- CV recency & planning settings: Current rating values are from the 2022 general revaluation and apply to rates from 1 July 2023–30 June 2026; the next revaluation is in 2025. Because CVs are fixed to their valuation date, they can lag when market conditions shift

Getting ready for valuation day — seller/owner checklist

Access & logistics

- Provide full access: keys, alarm codes, garage remotes, and safe access to all areas (subfloor/roof space if applicable).

- Pets & tenants: arrange pet containment and give tenants proper notice for inspection access.

- Timing: book a slot that allows daylight for exterior inspection and photos, and avoid overlapping trades on site.

Documentation to prepare

- Plans & consents: architectural drawings, building and resource consent numbers, Code Compliance Certificate (CCC) where applicable.

- LIM/building reports: the latest LIM and any independent building reports or producer statements (PS1/PS3/PS4).

- Title info: record of title highlighting easements/covenants/cross-lease flats plans.

- Recent work evidence: invoices, warranties (roofing, double-glazing, heating), compliance docs for electrical/gas work.

- Rental data (if investment): tenancy agreement, current rent, rental appraisal, expense summaries.

- Site potential: any subdivision feasibility, surveyed boundaries, or planning advice relevant to development capacity.

Property presentation

- Maintenance tidy-up: fix minor defects that could distract (leaks, broken latches, blown bulbs).

- Information labelling: clearly mark unconsented spaces as storage only; provide context if works are in progress.

- Chattels list: specify inclusions/exclusions to avoid assumptions in the report.

How to avoid re-inspections and delays

- Confirm scope early: clarify with the valuer whether it’s a desktop/kerbside or full inspection, and what documents they require up front.

- One package, one send: supply a single, well-organised digital pack (PDFs named logically) before the inspection.

- Answer queries fast: same-day responses to RFIs keep your report on track.

- Check critical dates: align finance/conditional dates with expected turnaround and any validity window your lender applies to valuations.

- Be transparent: declare known issues (weathertightness, unconsented works); surprises trigger re-visits or additional verification.

Why this matters

Councils revalue for rating on set dates; CVs are audited to national standards and may lag moving markets. A clean, well-evidenced file helps the valuer focus on current market value rather than chasing missing information.

FAQs

Q: What is a Free House Valuation in NZ, and who provides it?

A: It’s a no-cost estimate of likely market value intended for orientation and planning. Homeowners typically obtain one online or as part of an agent’s written appraisal; it’s not a formal valuation for lending or legal purposes.

Q: Do banks accept an agent appraisal?

A: No. An appraisal helps with pricing strategy and must reflect recent comparable sales, but lenders generally require a registered valuation for credit decisions.

Q: When will a lender insist on a registered valuation?

A: Common triggers include purchases, refinances, construction loans, low-deposit lending, and properties outside standard risk boxes (rural, unique, or newly built). The instruction method and report format must meet the bank’s policy.

Q: How accurate are online estimates versus formal valuations?

A: Online estimates are a valid first pass, but they can miss renovations, atypical layouts, or development potential. A registered valuation involves site inspection (when required), verified data, and comparable sales analysis, producing a defensible opinion of value.

Q: How long does a valuation take, and how long is it valid?

A: Straightforward jobs often complete in about a week once access and documents are ready; complex properties take longer. Validity is set by lender policy—commonly around three months, after which an update or new report may be needed.

Conclusion: Choose the right path with confidence

Free options are perfect for orientation and early decision-making; paid valuations are essential when lending, legal certainty, or complex properties are involved. Start with a clear baseline, assemble your documents, and align your timeframes with lender requirements so nothing falls through the cracks.

Ready for a reliable starting point? Get your personalised estimate at Price My Property.

{kind=link}

{kind=link}

{kind=link}

{kind=link}