Comparative Market Analysis NZ: What It Is And How It Works in 2026

If you are trying to work out what your home could realistically sell for, this guide is built for you. A comparative market analysis NZ does more than define a term. It needs to explain how appraisals work in New Zealand, how they differ from registered valuations and CV/RV figures, and how a seller can use comparable sales without getting misled by outdated or overly optimistic pricing. If you are selling through an agent in New Zealand, the written price appraisal must reflect current market conditions and be supported by comparable information, while your own site already positions homeowners around the three practical starting points: online estimate, agent appraisal/CMA, or registered valuation.

TL;DR

- A market appraisal or CMA is usually the best first step for a standard residential seller in New Zealand because it uses recent comparable sales, current listings, and local market context to estimate a likely sale range. See the REA appraisal rules.

- A registered valuation is different. It is a formal opinion prepared by a registered valuer and is often used when a bank, lawyer, court, trust, or dispute process needs a more formal report. See the Valuers Act 1948.

- CV/RV is a useful background, but it is part of the rating system and is not intended to serve as a current market-value guide for raising finance or insurance. See the Rating Valuations Act 1998.

- Online estimates can help you start your research, but official consumer guidance says they should only be treated as a starting point because they cannot fully account for condition or improvements. See official consumer guidance on settled.govt.nz.

- In New Zealand, before an agency agreement is signed, the agent must provide the seller with a written price appraisal that realistically reflects current market conditions and is supported by comparable information for similar properties.

Ready for a practical starting point? Get your FREE Market Property Report from Price My Property.

What is a market appraisal or CMA in New Zealand?

In New Zealand, ‘CMA’ can refer to a comparative market analysis in general use, while REA uses CMA to mean a current market appraisal. For most sellers, both terms describe the same evidence-based pricing exercise: comparing your property with recent sales, competing listings, and current local market conditions. In practice, many NZ homeowners experience this as part of a real estate agent’s market appraisal rather than as a separate document with different branding.

The Real Estate Authority says a current market appraisal must be explained to the vendor, including how the property compares to recent sales and how the appraised amount was reached.

What a good CMA usually includes

- Recently sold properties that are genuinely comparable

- current listings competing for the same buyers

- recent market sentiment in that suburb or buyer bracket

- adjustments for renovation level, condition, floor area, land use, outlook, parking, school zone, and layout.

- a realistic price range rather than one magic number

That approach aligns with both official REA expectations for comparable information and the practical, seller-focused framing already used on Price My Property.

Why sellers use a CMA before listing

Most homeowners are not asking for a theoretical value. They are trying to answer a practical question: “What could this property sell for in the current market?” That is why a CMA is so useful before listing.

It gives sellers a pricing range, helps them compare agents more intelligently, and reduces the risk of choosing the highest appraisal simply because it sounds flattering.

Is a CMA the same as a market appraisal?

For most readers, the honest answer is: close enough for practical use, but not always in wording. In NZ content, “market appraisal”, “agent appraisal”, “current market appraisal”, and “comparative market analysis/CMA” are often used side by side.

Is a written appraisal required when selling with an agent in New Zealand?

Yes. If you are selling through an agent, before an agency agreement is signed, the seller must receive a written price appraisal that realistically reflects current market conditions and is supported by comparable information about similar properties. REA’s agency agreement rules and settled.govt.nz guidance for sellers both reinforce this point.

If no directly comparable data exists, that should be explained in writing.

What this means in plain English

This matters because sellers are not supposed to be sold a fantasy number with no evidence behind it. A proper appraisal should be grounded in the real market, not just in what an owner hopes to hear or what an automated estimate happens to show.

REA also says it is not enough to hand over raw data; the licensee should explain why some sales were included, why others were excluded, and how the figure was reached.

Why physical inspection still matters

This is also why online tools have limits. A website can estimate value from data, but it cannot fully see presentation, deferred maintenance, quality of renovation, sun, privacy, smell, noise, or street appeal. Official NZ consumer guidance says online estimates are only a starting point, and REA says appraisals should not rely solely on electronic estimates.

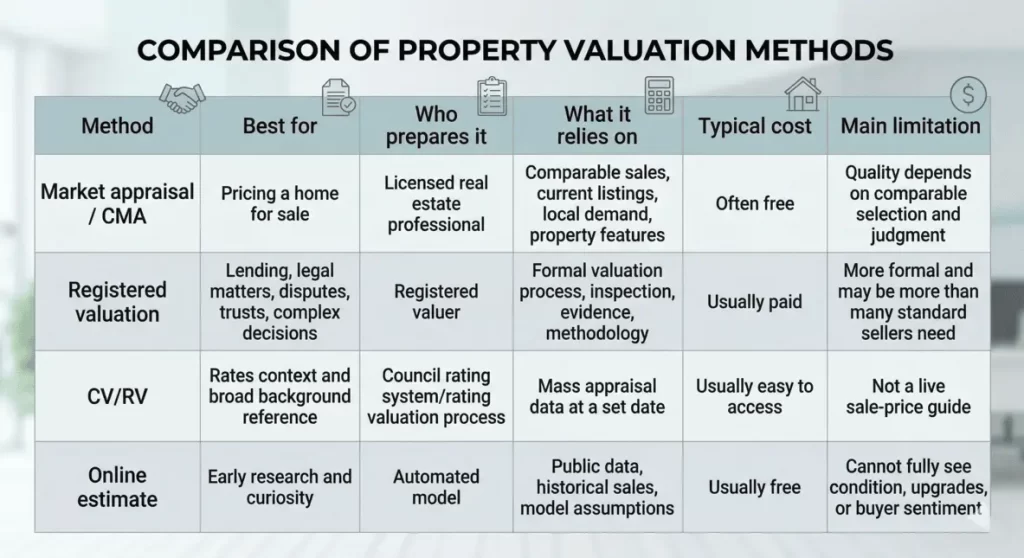

Market appraisal vs registered valuation vs CV/RV vs online estimate

Here is the simplest way to explain the landscape. A comparative market analysis NZ article must separate these four ideas clearly: a CMA or market appraisal helps you price a property for sale; a registered valuation is a formal professional valuation; CV/RV helps councils allocate rates; and online estimates are quick research tools, not final pricing decisions.

Quick comparison table

The table above reflects official NZ appraisal rules, the Valuers Act 1948 framework for registered valuers, and QV’s explanation that rating valuations are part of the rates system rather than finance or insurance valuation tools.

When to start with a market appraisal

For a standard homeowner thinking about selling, a market appraisal is usually the best first step. It is built to answer the sale-price question, it is often free, and it can quickly tell you whether the market supports your expectations.

If you want to compare the options before deciding on your next move, read Price My Property’s appraisal vs valuation guide.

When to pay for a registered valuation

A registered valuation becomes more important when someone besides you must rely on the number. That often includes a bank, lawyer, court, trust, estate matter, separation process, or a property type that is unusually complex or hard to compare. Settled. govt.NZ notes that a bank may require a valuation, and the legal framework for registered valuers sits under the Valuers Act 1948.

How does a CMA actually work?

At its best, a comparative market analysis NZ process works by selecting genuinely similar sales, adjusting for differences, checking live competition, and turning that evidence into a realistic range rather than an inflated promise. REA’s guidance emphasises not only comparable sales but also explaining why certain properties were included or excluded.

Step 1: Choose the right comparable sales

- in the same suburb or the immediate competing area

- sold recently enough to reflect current conditions

- similar in land size, bedroom count, bathroom count, parking, and property type

- similar in renovation level, presentation, and appeal

- subject to the same or similar buyer audience

Bad comparables create bad pricing. One superior sale on a better street can distort the entire range if it is not properly adjusted.

Step 2: Adjust for differences

- renovation quality

- layout and flow

- outlook, privacy, and sun

- site usability and development potential

- school zone and location nuances

- extra bathrooms, garaging, decking, or ancillary rooms

This is why a human appraisal often beats a simple model. The market pays differently for a tidy, well-presented home with stronger appeal, even when two properties look similar on paper.

Step 3: Check the current competition

Sold comparables show what buyers have paid. Active listings show what buyers are choosing between right now. A property can look “worth” one number based on past sales and still need sharper pricing if today’s buyers have more choice or weaker urgency. If you are still trying to pin down a likely range, use Price My Property’s guide to how much your house is worth in NZ.

Step 4: Turn the evidence into a realistic price range

The best result is usually a range, not an exact number. A range leaves room for presentation, buyer competition, timing, and method of sale. REA training material also refers to ending the appraisal with an appraised price or price range linked to the chosen comparables.

What makes an appraisal accurate?

The easiest way to judge a comparative market analysis NZ report is not to stare at the final number first. Judge the evidence.

The most accurate appraisals combine recent comparable sales, a physical view of the home, honest adjustments, and a realistic reading of buyer demand. That lines up with REA’s written-appraisal rules and with settled.govt.nz guidance that the agent should visit the property and support the estimate with similar sales.

The seven things that improve accuracy

- Recent comparable sales rather than old market evidence

- Like-for-like property selection

- Clear explanation of why each comparable was chosen

- Real inspection of the property’s condition

- Smart adjustment for upgrades and shortcomings

- Awareness of what buyers are choosing now

- A sensible range instead of one aggressive number

Red flags that should make a seller cautious

- only one or two comparables

- Reliance on old sales in a changing market

- No inspection of the actual home

- a number that feels flattering but unexplained

- no discussion of active competition

- no adjustment for obvious differences

- heavy reliance on online tools alone

Want a reality check before trusting an automated figure? Get a FREE Market Property Report from Price My Property and compare the range with recent local evidence before you make a pricing decision.

How to read a CMA like a smart seller

Do not read the last page first and stop there. A proper comparative market analysis NZ report should be judged by the quality of its comparables, the logic of its adjustments, and whether the recommended range actually matches the current market.

REA’s own guidance stresses that the seller should understand how the property compares to recent sales and how the amount was reached.

What to look for in the report

- How many comparable sales were used

- When those sales happened

- whether the comparables are truly similar

- What the appraiser says about condition and presentation

- How active listings are affecting the likely range

- whether the report explains why some evidence was excluded

- whether the suggested method of sale fits the likely buyer pool

Questions a seller should ask the agent

- Why did you choose these comparables?

- Which sales did you reject, and why?

- What would move your range up or down?

- Where do you think the main buyer pool sits?

- Does the method of sale change the price strategy?

- How would you price it if the market softened next month?

- What would make you suggest I pay for a registered valuation instead?

The most common seller mistake

The most common mistake is choosing the highest appraisal rather than the best-supported one. An unrealistically high appraisal can be expensive if the property is incorrectly priced from the start.

Common pricing mistakes a CMA helps you avoid

A good CMA does not just tell you a number. It protects you from predictable pricing errors.

Mistake 1: treating CV or RV as your asking price

CV/RV is part of the rating system. It can be a useful point of reference, but QV says rating valuations are used to help allocate rates, are set at an effective date, and are not designed for finance or insurance valuation purposes. That alone is enough reason not to use CV/RV as your list-price shortcut.

Mistake 2: assuming your renovation added dollar-for-dollar value

Some improvements add strong market appeal; others do not fully return their cost. The market rewards buyer usefulness and presentation, not just spend. That is why comparable evidence matters more than renovation invoices alone.

Mistake 3: copying the neighbour’s result without context

A neighbour’s sale may have had better timing, a better site, a stronger presentation, or more competition. Good pricing always asks whether the property is comparable, not just nearby.

Mistake 4: relying on online estimates alone

Online tools are useful, but official guidance says they should only be used as a starting point because they cannot fully assess the condition or improvements.

Mistake 5: choosing the wrong sale method for the pricing evidence

Some homes suit auction, some suit negotiation, and some need more flexible buyer discovery. Pricing and method of sale should work together rather than being treated as separate decisions.

When should you get a CMA or market appraisal?

You should get one when you are thinking seriously about selling, comparing agents, testing whether your expectations match the market, or deciding whether a paid valuation is actually necessary. Settled.govt.nz repeatedly presents current market appraisals as one of the practical ways sellers can work out value before making bigger decisions.

Before you list

This helps you choose a likely buyer bracket, a pricing method, and the right expectations before the campaign starts.

Before you compare agents

This is one of the smartest uses of an appraisal. It lets you compare evidence quality, not just personalities or promises.

Before you pay for a valuation

Many homeowners do not need to jump straight to a paid valuation. In a standard sale, a market appraisal may first answer the key question.

When you are curious but not ready

A homeowner who is six months away from selling still benefits from a grounded market range, especially if they are deciding whether to renovate, refinance, or move.

If you are deciding whether a free appraisal is enough, see Price My Property’s guide “How to Get a Free House Valuation in NZ,” which explains when a free appraisal is enough and when a paid, registered valuation may be more appropriate.

Frequently asked questions about CMAs, appraisals, and property value in NZ

Q: What is a comparative market analysis in New Zealand?

A: A comparative market analysis NZ report is a market-based estimate of what your property could sell for using recent comparable sales, current listings, and local buyer conditions. In practice, many homeowners receive it as part of a market appraisal from a licensed real estate professional. REA requires appraisals to be explained to the vendor and supported by comparable evidence.

Q: Is a CMA the same as a market appraisal?

A: Usually, yes, for practical seller purposes. In NZ content, the terms are often used together or interchangeably, even though one site may say “market appraisal” and another may say “CMA”.

Q: Is a written appraisal required before signing with an agent?

A: Yes. The seller must receive a written price appraisal that reflects current market conditions and is supported by comparable information. If comparable information is not available, that should be explained in writing.

Q: Is a CMA the same as a registered valuation?

A: No. A CMA, or appraisal, is a sales-pricing tool. A registered valuation is a formal valuation prepared by a registered valuer and is more likely to be needed for lending, legal, or dispute purposes.

Q: Can an online estimate replace a CMA?

A: No. It can help you start your research, but official guidance says it should only be used as a starting point because it cannot fully account for condition, improvements, or property-specific appeal.

Q: Is CV or RV the same as market value?

A: No. Rating valuations help councils allocate rates and are effective from a specific date. They are not designed to be live market pricing tools for lending or insurance.

Q: How much does a property appraisal cost in New Zealand?

A: Many standard residential appraisals are free when you are considering selling. Several NZ agency pages explicitly advertise free property appraisals or free current market appraisals for vendors.

Q: How much does a registered valuation cost?

A: Costs vary by region, urgency, property type, and complexity. The safest general rule is that a registered valuation is a paid service, and the quote will vary depending on the level of detail and the property involved.

Q: How recent should comparable sales be?

A: There is no single universal cut-off, but the evidence should be recent enough to reflect current market conditions. In a fast-moving market, older evidence becomes less reliable more quickly.

Q: What happens if there are no directly comparable sales?

A: The agent should say so in writing and explain the limitation. That is reflected specifically in REA guidance and appraisal rules.

Q: Can I do my own CMA?

A: You can research recent sales, listings, and suburb evidence yourself, and that can be useful. But a DIY estimate will usually be weaker than a proper appraisal because it is harder to select the right comparables, adjust for differences, and accurately gauge buyer sentiment.

Q: When should I pay for a registered valuation instead?

A: Pay for one when a bank, lawyer, court, estate, trust, or dispute process needs a formal valuation, or when the property is unusual enough that a standard appraisal may not be enough.

Q: What should I ask an agent during an appraisal?

A: Ask why they chose the comparable sales, what they adjusted for, what would move the range up or down, how current listings are affecting demand, and whether they think the method of sale changes the likely outcome.

Q: How can I tell one agent’s appraisal is better than another’s?

A: The better appraisal is usually the one with stronger comparable evidence, clearer reasoning, more honest adjustment for differences, and a range that feels realistic rather than flattering.

Conclusion

For most standard residential sellers, a comparative market analysis NZ approach is the most practical way to price a home properly. It gives you a realistic sale range based on evidence, helps you compare agents intelligently, and keeps you from confusing market price with CV/RV, an automated estimate, or a formal valuation.

When you are ready to act, get your FREE Market Property Report from Price My Property to review the evidence and decide whether you should list, compare agents, or pay for a formal valuation.

{kind=link}

{kind=link}

{kind=link}